Touted as the world’s third largest emitter of greenhouse gas, India is steadily on its way to transition from fossil fuels to renewable energy. The targets that the country has set itself are closer to being achieved and even surpassed. Sadia Sohail explains the newest study on India’s energy policy.

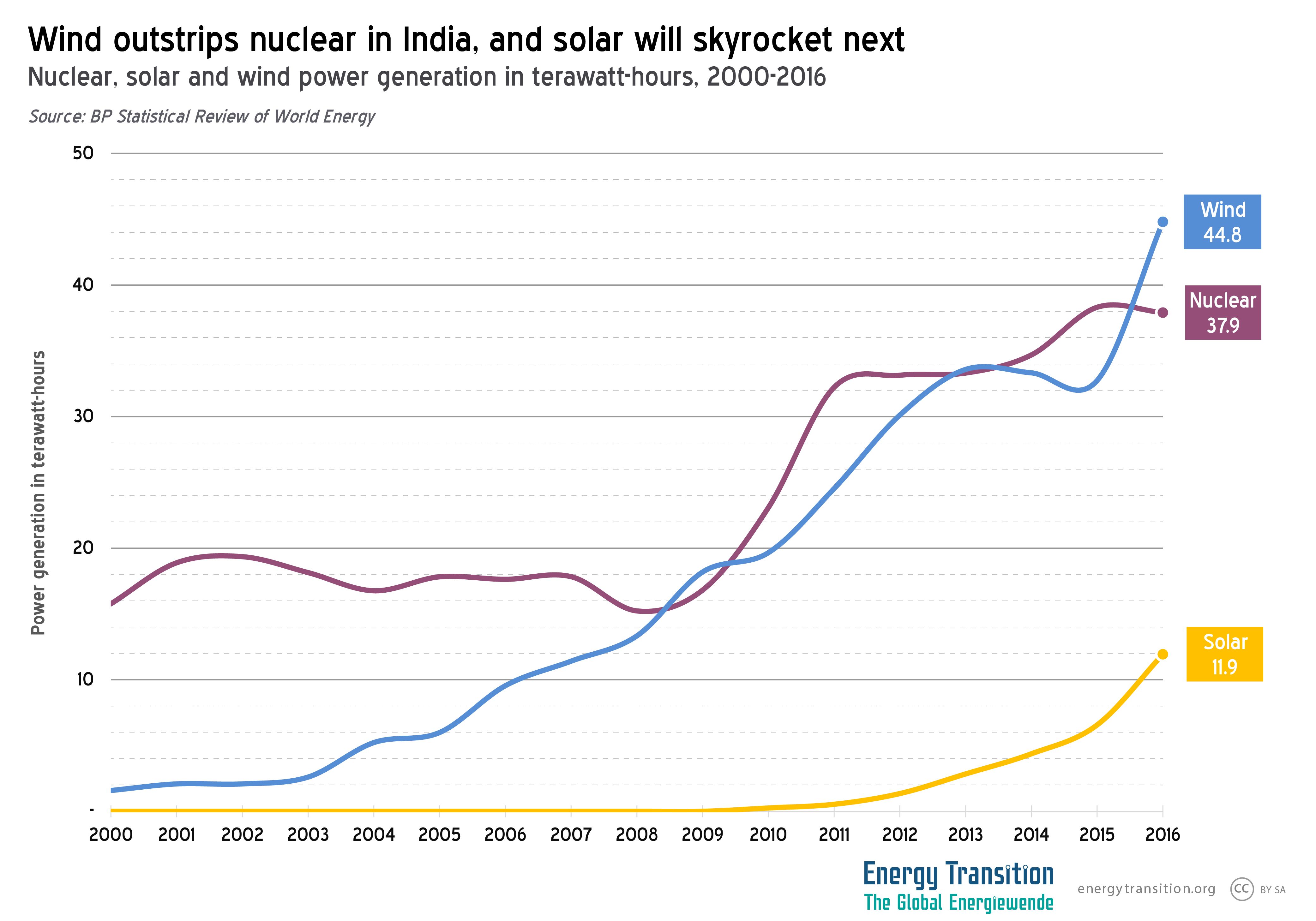

India’s wind power has outstripped nuclear, and should hit 60GW by 2022 (Photo by Vigneshvicky, edited, CC BY SA 4.0)

The government policy intends to achieve 175 GW of installed renewable energy capacity by 2022. Of these, 100 GW will be from solar, 60 GW wind energy, 10 GW small hydropower and 5 GW of biomass based power projects. At the end of first quarter of 2017, about 59 GW are installed according to official figures.

Furthermore, India’s commitment in the UNFCCC process includes achieving 40 per cent of electrical power from non-fossil sources by 2030. As the current figure stand already at about 31 per cent, this latter target is likely to be superseded, although it needs to be noted that large-scale hydro as well as nuclear power is included here, i.e. energy options not generally compatible with sustainability concerns.

Over the last decade, electricity capacity and power generation in India have continued to grow at a fast pace. The country’s installed electricity capacity increased at a cumulative annual growth rate of 9.3 per cent, while generation grew at 6.6 per cent; renewable energy exhibited even faster growth in the past decade, at a cumulative annual growth rate of 20 per cent.

The brave new world

India is looking at a new, brave world of renewable energy. For the first time since the climate talks started in 1992, there has been a market shift that indicates the potential to decarbonise the energy sector in the country. The current market trends show that the renewable energy costs have come down significantly in the last 10 years; solar photovoltaic (PV) costs have reduced by 20% annually since 2007. Projections on future costs indicate that solar PV will be the cheapest source of electricity in India by 2020 and solar rooftop system with battery back-up will achieve grid-parity by 2025.

The policy environment in the country is also conducive to the renewable energy sector. A preferential tariff and subsidy programme for renewables, concessions given by several states for reduced transmission and distribution charges are among several policy initiatives that have contributed to the considerable growth of the sector in the country. In addition, Renewable Purchase Obligations require electricity distribution companies to purchase a percentage of power from renewable sources.

Tariffs have been one of the most important factors in pushing renewable energy forward. State Electricity Regulatory Commissions give preferential tariffs for renewable energy. This preferential tariff is based on a cost plus formula that allows generators a reasonable rate of return on their investments. Wind power in India developed primarily on the basis of preferential tariff, which incentivised developers to install more wind power plants.

Unlike wind power, solar power in India has followed the route of competitive bidding. Competitive bidding has allowed solar power tariffs to decrease from Rs 12/kWh in 2010 (19 cents per kWh) to around Rs 3/kWh (5 cents per kWh) today.

Apart from preferential tariffs, India offers a number of other financial incentives for renewable energy projects. These include tax holidays of up to 10 years and accelerated depreciation of up to 80 per cent in the first year. There are excise and custom duty exemptions for most of the imported equipment, machinery, etc. For open access renewable energy projects – where renewable power can be sold to any customer – concessions have been granted on transmission and distribution charges.

The big picture

In a bid to curb emissions, India’s Central Electricity Authority is also in the process of phasing out coal-fired power plants which are more than 25 years old on the basis of their ‘inefficiency and un-economic operation.’ Several plants will also be retrofitted. The draft National Electricity Plan also goes on to state that no extra coal power stations will be needed until at least 2027 beyond the generation capacity of 50 GW that is under construction. It is estimated that coal consumption in the power sector in India could peak by 2030 and at a much lower level than expected. In addition, in the 2030s, most of the installed capacity of the power sector will come from non-fossil fuels.

It is also estimated that between 2016-17 and 2031-32, for every 1 MW of coal power plant installation, 4.5 MW of solar and wind capacity will be installed. With solar power tariffs for larger projects hitting as low as Rs 3/kWh (5 cents per kWh), decreased wind power tariffs, and improved storage technology, it will be a no-brainer for stakeholders to set up a new solar or wind power plant compared to a new coal power plant. Renewable energy is thus becoming the most important energy sector in the country and will drive the energy industry in the future.

However, while the country is leapfrogging in its energy transition, it is not enough to just look at the installed capacity and output. Massive finance still needs to be provided. Even though the cost of renewable energy has reduced, the total amount of money required to meet the targets remains high. Similarly, electricity distribution companies will have to rise to the occasion by introducing reforms to support renewable energy. Grid stability and changes in infrastructure, as well as forecasting and scheduling for renewables, will also be important factors in determining the pace of India’s transition.

Sadia Sohail is the coordinator for the Resource Governance Programme at the Heinrich Böll Foundation India. She has also worked as a Senior Research Associate at Centre for Science and Environment (CSE) a public interest research and advocacy organization based in New Delhi.

Excerpts from the report ‘India’s Energy Transition: Potential and Prospects’ published by Heinrich Boell Foundation and Christian Aid, India

It’s a baffling choice by India to exclude large-scale hydro from the definition of renewables. Of course it’s sustainable, barring climate catastrophe cutting the runoff from the Himalayas. Dams are built to last for centuries. It is quite true that (a) the construction of large reservoirs often destroys large areas of valuable farmland or forests, and disrupts the human communities that live from them, (b) that the good sites have mostly already been taken. New big hydro is therefore not a good candidate for the new capacity needed. However, the large hydro legacy ideally complements wind and solar, in India as elsewhere. It is highly despatchable, with no “must-run” constraints, has negligible running costs, and can easily be retrofitted for pumped storage if needed.

The volume of coal plants under construction in India is now significantly less than 50 GW. Coal Plant Tracker listed 43 GW of active construction as of last July. Cross-checking their list against Wikipedia’s page on troubled Indian coal construction sites, I found that four of the projects that were active in July, totalling 3.7 GW, had dropped out by December. The current total is therefore close to 39 GW. Wait for the next update from Coal Plant Tracker.

The economics of new coal plants are disastrous in India (link to Forbes article). New wind and solar is selling for under the average cost of thermal coal electricity. Despatch priority for the former, and slower than expected growth n demand, have driven coal plant capacity factors down to 57%, which is much less than what the investors planned on getting.

It would be nice to see and update on the above feature because we are now in 2021 and at least if we get data for 2020 it will is very useful that is not to you say that the above article is off less use it was certainly very useful