In a recent study, Berlin-based think tank Agora Energiewende estimated future cost impact of renewable electricity in Germany. One of the assumptions deserves more attention: the shrinking of net onshore wind growth. Craig Morris investigates.

Will repowered wind turbines be pushed out of the feed-in tariff? (Photo by Dirk Ingo Franke, CC BY-SA 3.0)

If you speak German and want to play around with the numbers behind Agora’s study (the main finding of which I covered here) to see how different outcomes would change the cost, Agora provides an Excel table. Strangely, at first glance, it seems to include an error. I contacted the organization, and its press spokesperson Christoph Podewils confirmed, however, that there is no error. The study assumes that net capacity additions for onshore wind will shrink dramatically.

My colleague Thomas Gerke pointed out that the researchers from the Öko-Institut (German Institute for Applied Ecology), who conducted the study for Agora, seem to have included gross growth numbers for onshore wind (see the screenshot below), whereas the target specified in the amendment of the Renewable Energy Act last summer is clearly 2.5 GW net. In particular, as the announcement last year by the German government (in German) explains, when new wind turbines replace old ones, only the additional capacity (the new turbines minus the old ones) is counted towards that target. So if 3 GW replaces 0.5 GW, then only 2.5 GW is counted.

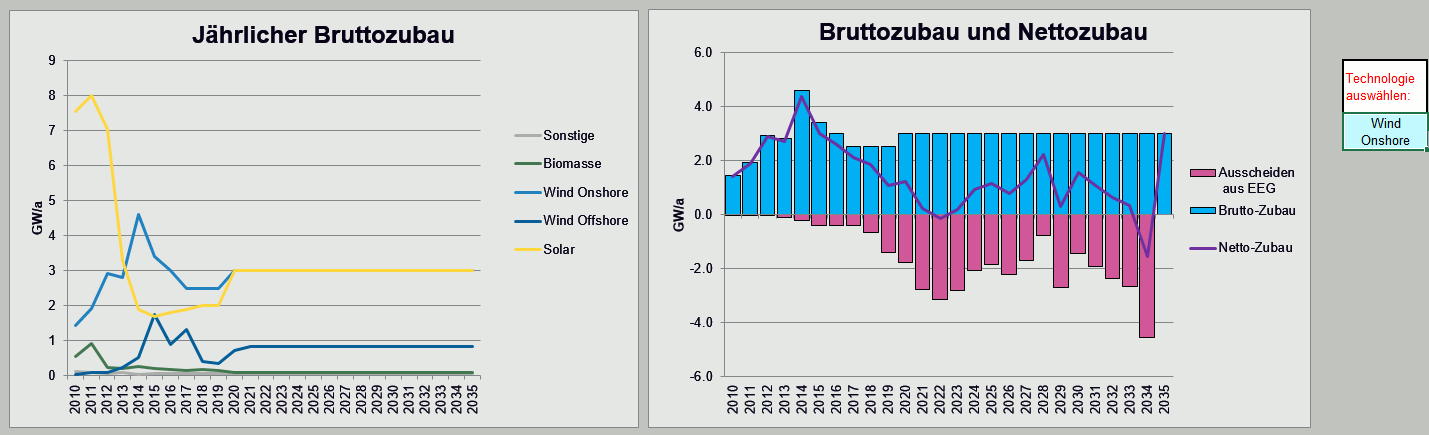

Here is the chart from Agora’s Excel table:

On the left, we see that 3 GW of onshore wind (hidden by the overlapping yellow line for solar) is constant starting in 2020 after the market returns to 2.5 GW in a couple of years. The chart on the right represents gross added capacity above the baseline (blue bars) and retired systems below the baseline (red bars). The line through the middle shows the net additions, which actually reach nearly 0 around 2022 – and go negative in 2034.

Podewils points out that the corridor only applies up to 2017, when Germany plans to switch to a system of auctions, potentially getting rid of feed-in tariffs entirely. He adds that “the corridor would then be largely obsolete” because the government could then specify exactly how much should be built.

If the German government sticks to its current target, Podewils explains, the 4.4 net GW built last year would need to be replaced, with an additional 2.5 (the current government’s target) added on – bringing the total up to 6.9 GW. “We believe that is not very probable,” Podewils explains. Here, Agora points out that the current policy would require ever greater onshore capacity – even though the government would reach its renewable power targets under the scenario investigated.

For what it’s worth, the German grid regulator has modeled the continuation of the current corridor (in German) – exactly what Agora thinks is unlikely – up to 2035. The grid experts call this expectation “the upper limit of what is probable”. So it seems that those organizations are indirectly signaling that the current annual target might need reducing.

Extrapolated to 2035, 88.8 GW of onshore wind would then be installed – only slightly above the 87 GW that German researchers at Fraunhofer IWES believe will be needed for a 100 percent renewable electricity production by 2050. In other words, Germany does not need that much, so its current net annual growth target for onshore wind is generous – but lowering it will be politically challenging. (Keep in mind that estimates for how much onshore wind power is needed depend on how much other stuff is built, and those figures also vary.)

One could argue, of course, that a stable market of 3 GW (as modeled in the study starting in 2020) would be welcome. Indeed, turbine manufacturers might be happy enough, but would wind farm owners? In some of these years, the policy would almost constitute expropriation; some wind farm owners would not be able to replace old turbines, but they would also no longer be eligible for feed-in tariffs. One main option for these wind farm operators who cannot rebuild would be to sell electricity from their old turbines on the wholesale exchange, but both wind and solar power will make themselves worthless on the wholesale market because prices will drop when most of this electricity is generated.

Politically, what Agora models here is therefore unlikely. German states resisted the original proposal of a gross figure, which is why we got a net target last year. Agora focuses on technical necessities and finds that a calculation of gross annual additions will allow Germany to reach its targets; the study does not investigate the political feasibility of this arrangement. I doubt that the wind farm operators who got this grassroots Energiewende going would accept this proposal.

In my next post, I investigate this issue further in terms of what I call “legacy solar power.”

Craig Morris (@PPchef) is the lead author of German Energy Transition. He directs Petite Planète and writes every workday for Renewables International.

“Extrapolated to 2035, 88.8 GW of onshore wind would then be installed – only slightly above the 87 GW that German researchers at Fraunhofer IWES believe will be needed for a 100 percent renewable electricity production by 2050.”

IWES assumes a quite low demand for electricity. If you want reserves for unexpected demand (higher heat demand of buildings or industry), more than 90 GW onshore wind would be useful.

With 30 years life time of a turbine, 120 GW onshore wind would require around 4 GW gross installation per year, 150 GW around 5 GW gross installation per year. Net installation would be of course zero at the end of 30 years.

Onshore wind is the cheapest source of RE, why not aiming at higher numbers.

Discussion of the steady state situation, i.e. annual gross installation, would be more useful IMHO than working with confusing annual net additions.