Two items that make up more than 10 percent of the German renewables surcharge could shrink considerably over the next year, possibly enough to keep the surcharge from rising further. Whether retail power prices rise or fall, however, depends on more factors than simply this surcharge.

The renewables surcharge might stop rising – and positively affect retail power prices. (Andreas Morlok / pixelio.de)

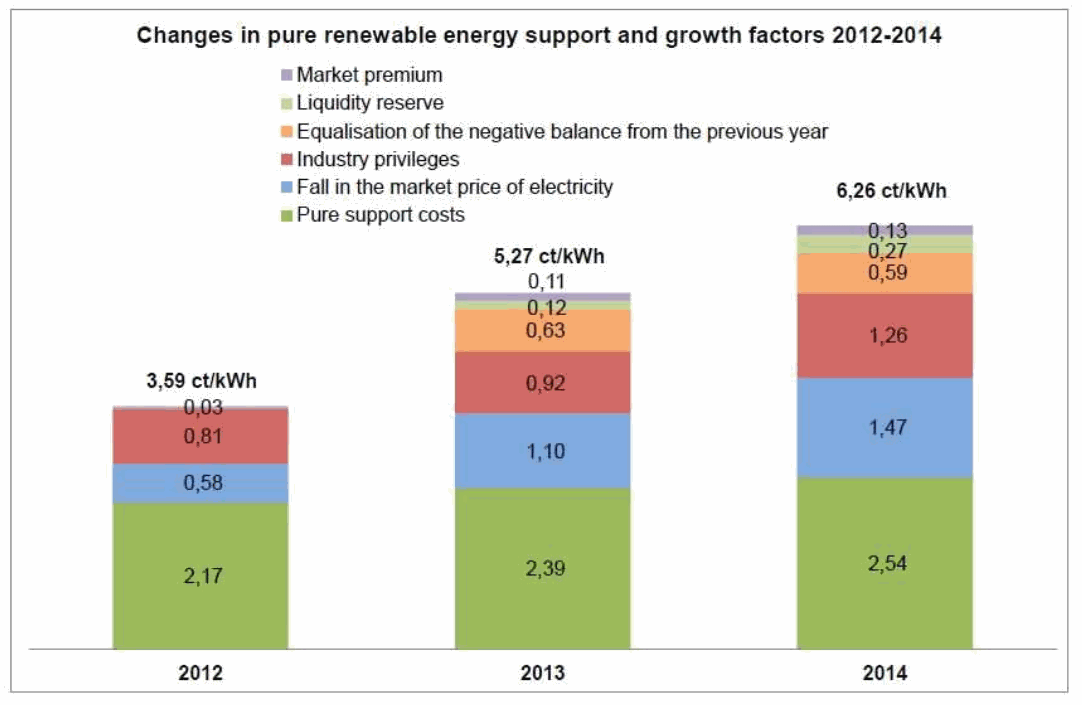

German renewables lobby group BEE recently produced a wonderful paper in English (PDF) explaining the EEG surcharge, which I call the renewables surcharge. Today, I want to focus on just one of the charts showing the evolution of this surcharge since 2012.

Two of the items here are related to costs carried forward, meaning that there was a shortfall. Back when PV was pretty expensive and started to boom (around 2009), more money was paid out as feed-in tariffs to producers of green power than was taken in from the surcharge, which is estimated for a calendar year. Part of the increase over the past few years has therefore been related to working down this backlog and preventing a new shortfall.

Two of the items here are related to costs carried forward, meaning that there was a shortfall. Back when PV was pretty expensive and started to boom (around 2009), more money was paid out as feed-in tariffs to producers of green power than was taken in from the surcharge, which is estimated for a calendar year. Part of the increase over the past few years has therefore been related to working down this backlog and preventing a new shortfall.

In 2013, 0.63 cents (orange area in the chart) went to paying down that debt, with 0.12 cents set aside to cover a potential new shortfall. But it now seems that the days of a shortfall are over. At the end of 2013, the EEG budget was “only” 225 million euros in debt (see page 1 of this PDF in German). That may sound like a lot, but the shortfall at the end of 2012 was nearly 2.7 billion.

Source: EEG/KWK-G.net

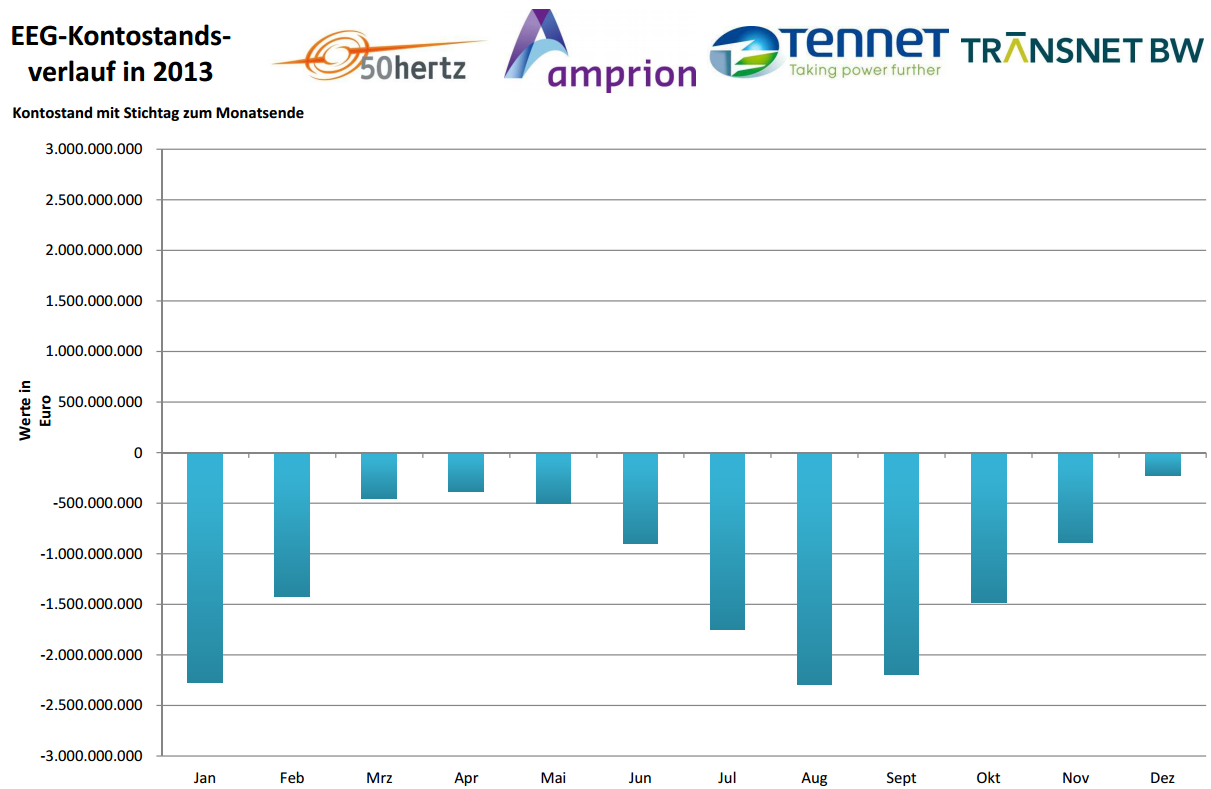

Going forward, we see in the chart below that the overall balance will probably enter the black in January. Typically, the deficit has decreased considerably in the winter, when a lot of wind power but little solar power is generated; as a result, the deficit reaches its maximum around August/September. But draw those bars upwards from the -225,000,000 in December, and we will be in the black, possibly until July – and, more importantly, for the year as a whole. By the end of the year, there may no longer be any need for the “equalization” (orange area in the BEE chart above) or the “liquidity reserve”, which made up 14.2 percent of the renewables surcharge in 2013 and 15.3 percent in 2014. Indeed, those two items alone amount to 0.96 cents in this year’s renewables surcharge, nearly equivalent to the entire increase of 0.99 cents.

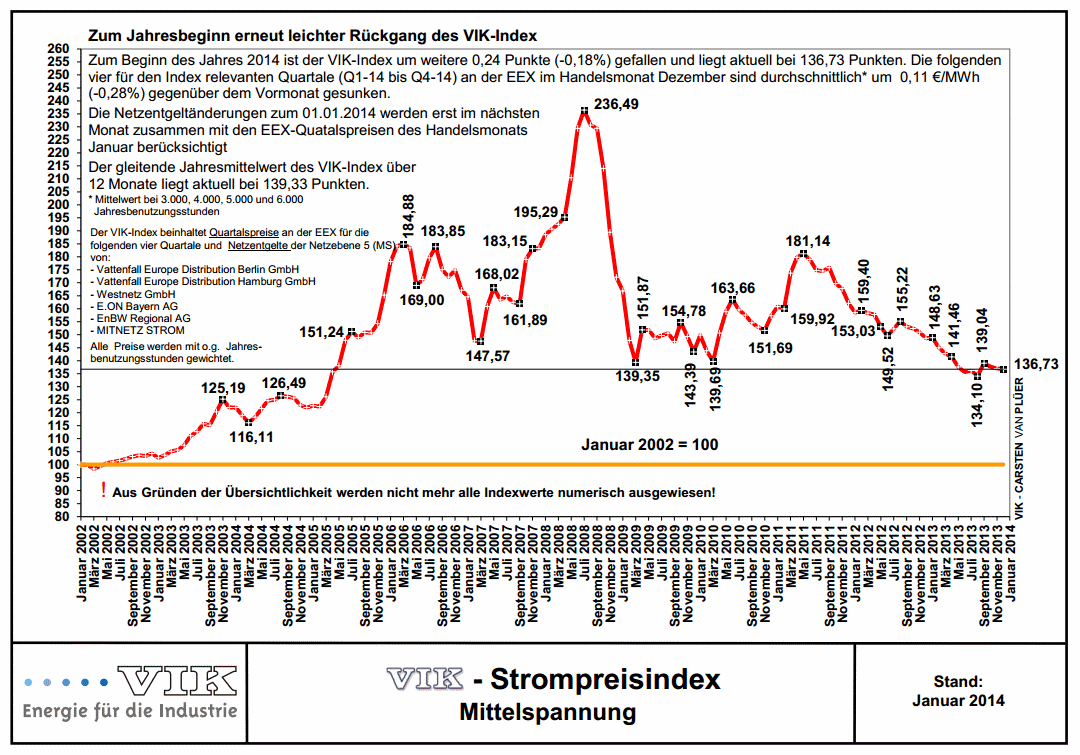

Remove those two items and you therefore return to a surcharge at the level of 2013. The “industry privileges” (red area in the BEE’s chart above) are also expected to be drawn down, which would lower the surcharge even further. On the other hand, wholesale prices continue to drop, which will provide the opposite effect (blue area). In Q4 2013, the average baseload power price fell by 3.2 percent to 3.754 cents below Q3. And as the chart below shows, the VIK index of industry power prices has reached a level (in absolute terms, not adjusted for inflation) not seen since May 2005. Overall, the result could be a lower surcharge and slightly lower retail rates.

The findings are especially interesting in light of the recent McKinsey report (unpublished, but here is a summary in German), which found that the government’s plans to reduce the feed-in tariffs for wind power would only reduce the surcharge marginally by 0.03 cents. In contrast, McKinsey found that a revocation of the industry exemptions to a realistic level could lead to a 0.7 cent reduction.

Craig Morris (@PPchef) is the lead author of German Energy Transition. He directs Petite Planète and writes every workday for Renewables International.