Why does Germany, a country with the same amount of sun on a yearly basis as Alaska, have residential solar costs half that of the U.S.? Why have solar panel prices dropped significantly while whole-system cost has remained relatively high? For Dan Seif, principal with Rocky Mountain Institute’s electricity and industrial practices, and Jesse Morris, Senior Associate for electricity and transportation practices at Rocky Mountain Institute, the answer lies in the soft costs of solar PV—all the non-hardware-related costs of installing a solar PV system.

Hardware costs for PV have gone done dramatically. The next challenge will be lowering soft cost. (Photo by CoCreatr, CC BY-SA 2.0)

To bring down the costs of solar PV in the U.S., RMI implores the solar industry to dedicate some energy away from the rallying points du jour (net-energy metering and the investment tax credit), which may only have short-term benefits, and focus on efforts that will make PV most competitive in the long run—reducing soft costs. RMI has had an institutional focus on lowering soft costs since 2008, including prominent, RMI-led multi-stakeholder workshops and substantial research and engagement with developers/financiers, installation contractors, equipment designers, city governments, and utilities. With the new release of our soft cost roadmap report with the National Renewable Energy Laboratory (NREL), RMI has charted a path to guide soft cost reduction.

U.S. soft costs remain exorbitant

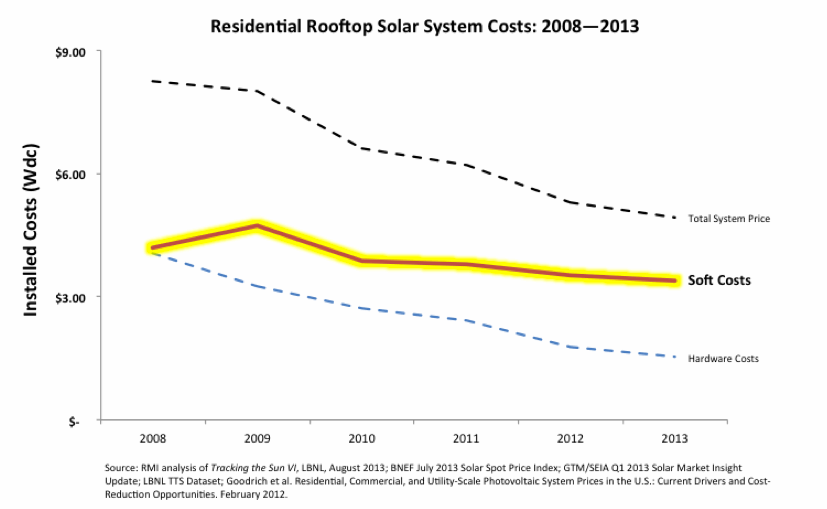

As the chart illustrates, progress on soft costs has been modest, and particularly unimpressive when compared to hardware cost reductions.

Unfortunately, even the residential “total system price” shown above, and its apparent sharp rate of decline, is poor compared to our international peers. Australia and Germany, both with healthy solar markets, have residential solar costs at about half that of the U.S. What’s more, nearly every penny of the savings in upfront capital costs in those countries is due to much lower soft costs. In brief, soft costs have become a national embarrassment.

Framed more concretely, in the U.S. you could give away solar panels for free and still end up paying nearly $20,000 for a residential system. That may seem absurd, but it’s our current reality. Continuing cost reductions on the module and hardware side of the solar equation will help solar become more widespread, but the real cost-reduction potential is on the soft cost side. And these costs must come down drastically if we are to attain Reinventing Fire’s vision of a more distributed, resilient, and low carbon (80 percent lower carbon dioxide emissions) electrical system (which, combined with other energy sector advancements addressed in Reinventing Fire, provide a $5 trillion (2010-$) net present value uplift to the U.S. economy).

Roadmap Summary Findings

In 2011, the U.S. Department of Energy launched the SunShot Initiative, to make solar energy cost competitive with other forms of electricity by 2020. NREL and RMI’s roadmap shows how we can reach SunShot cost goals—to reduce the cost of solar energy systems by approximately 75 percent—from 2013 to 2020. This roadmap report was compiled with over 70 industry interviews and also supported with prior research by NREL, RMI, and outside sources.

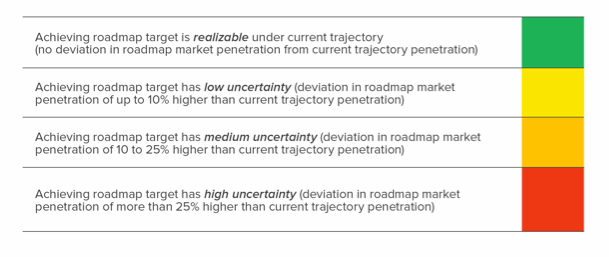

As shown below in color code, we’ve got a tough slog ahead of us on soft costs in both the residential and small (<250 kW) commercial markets. Achieving installation labor and permitting, inspection, and installation (PII) targets are the most challenging and uncertain, but reducing financing and customer acquisition costs to 2020 targets won’t come without a lot of innovation, sweat, and tears. Today we will cover what needs to be done to lower PII and customer acquisition costs. Tomorrow in part 2, we will describe the necessary steps to reduce financing and installation labor costs.

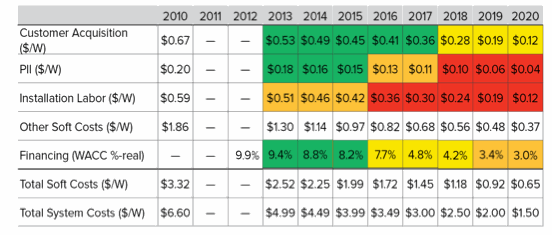

Residential PV Summary Roadmap

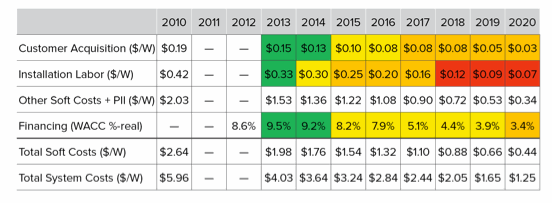

Commercial PV Summary Roadmap

While roadmapping for the targeted soft costs (those color-coded above) is important and long overdue, we acknowledge that the “other soft costs” category, where profit, transactional, asset management, margin, and assorted overhead costs live, is now the largest dollar per watt cost category. We’re happy to announce that NREL is now diving into this cost category, but benchmarking had been lacking to date. Since profit is typically observed as a percentage of total deal amount, reducing soft costs like customer acquisition and installation labor will help to reduce this large “other” category. However, outside of these dynamics, there still should be significant roadmapping and on-the-ground (…or in the corner office) efforts to help better understand and reduce this major cost component as soon as possible.

What are the tools for solving this puzzle?

Permitting, inspection, and interconnection (PII)

In regards to PII, Germany is currently living on a much more solar-favorable planet than us here in the U.S., even though the country as a whole only gets about the same amount of sun as Alaska each year. In Germany, only one form—the feed-in tariff registration form—with generally no inspections (audit only) and just one necessary approval (interconnection) are required to manage the bureaucracy of installing a grid-connected residential PV system. A similar, bureaucracy-light situation across the entire U.S. would require massive landscape change. Nevertheless, several near-term opportunities exist that could achieve modest cost reductions in existing markets while, more substantially, moving other U.S. markets out of stuck/marginal positions. This roadmap report did not examine commercial PV PII, as quality benchmarking of PII costs for commercial projects thus far is not yet available.

For residential PII, some tools for improvement are:

- Improved standardization: Standard, reasonable practices could go a long way toward reducing installer challenges in managing jurisdiction-by-jurisdiction differences. Vermont’s PV registration model, for installations of 10 kW and smaller, exemplifies a standardized, streamlined PII process.

- Improved transparency: Easy to use, comprehensive, and correct databases laying out all of the major PII considerations for all U.S. jurisdictions should help solve installer headaches. Clean Power Finance launched a national PII database, which is a great step in this direction, though it’s yet to be proven that this wiki-based platform is the full answer.

- Online permitting: The time traveling to and from permitting offices, as well as waiting time once there, can be diminished if solar permitting were done online.

Unfortunately, the full solution set to get to roadmap targets in the U.S. for PII is not completely known. NREL and RMI’s research left a noticeable $0.07/watt gap for PII requiring an “undefined” solution.

Customer acquisition

Customer acquisition costs are much more than just the advertising, marketing, and deal-closing costs associated with getting systems installed. They include the costs of dead deals that must be spread across successful ones, as well as the costs of customized designs to appease customers. While customer acquisition costs represent about 10 percent of deals in both residential and commercial markets, they are still painfully high compared to Germany and Australia. The good news (from preliminary NREL 2012 benchmarking data) is that these costs are coming down a bit. What’s more, this is a very active entrepreneurial space, and in the residential market customer acquisition appears to have the most certain path to its roadmap target of all soft cost categories.

Here are some of the more impactful tools:

- Software assessment: For residential installs, increased and improved use of software based site-assessments, particularly those that generate customer quotes, should produce better and lower cost quotes, increasing the chance of locking down customers and negating the need for costly in-person visits to the home.

- Referral programs: Referral programs, like SolarCity’s, are perhaps the only “tried and true” method of increasing residential solar adoption. Without the trusted brand recognition other industries benefit from (GE, Maytag, Sony, etc.), referring through friends, neighbors, or other community sources is key to enabling trust in the sales process. There are many grassroots solar familiarization efforts and referral-based business models (e.g. Solarlist introduces you to solar through your local college students), but they’re a bit immature at the moment. Maturation of such efforts and the ability to be broadly effective across new and existing markets will be critical.

- Consumer awareness programs: We solar advocates love to email each other links to the funny SunRun commercials on YouTube, but that’s much more the exception than the rule. There just isn’t much mainstream advertising and marketing out there, and most consumers are still largely in the dark. TV commercials might not be the answer (one author just disconnected his cable…), but effective customer education and familiarization is nevertheless important. In fact, it seems to be at least $120 million important to SolarCity, who for that amount recently purchased the direct marketing firm Paramount Energy Solutions, LLC.

- New commercial markets: For the small commercial market, the majority of customers are either laying out cash or garnering financing thanks to their very high credit quality (large corporations and municipal/county-backed entities like hospitals, schools, etc.). Without broader financing, the small commercial market will remain a minor part (currently less than 10 percent) of the overall U.S. solar market. Innovative financing structures can potentially unlock this market (e.g., Commercial PACE, specialty property rights/easements, and real estate investment trusts (REITs)), but finance alone won’t be enough. The customer outreach component will be equally critical. For PACE and other market-expanding financial tools, engagement solutions that match well with their intended customer bases are need. What those exact solutions will be, we frankly don’t know, but sharp minds are needed to sort this out.

Reducing permitting, inspection, and interconnection costs and lowering customer acquisition costs are key to bringing down the cost of solar PV. As you might imagine, they also can influence each other. Cold feet would likely sink in if we all shook hands with a salesperson at our local car dealership on terms for a new car, and the dealer said, “Come back in eight weeks and we’ll finalize the deal.” Similar dead deal issues persist from potential solar customers waiting through long permitting processes. Therefore substantial improvements in one soft cost might help synergistically solve others.

Coming in part 2 we will explore how to reduce two other soft costs: financing and installation labor.

This article was written by Dan Seif, principal with RMI’s electricity and industrial practices, and Jesse Morris, Senior Associate for electricity and transportation practices at Rocky Mountain Institute, and first published at RMI Outlet.